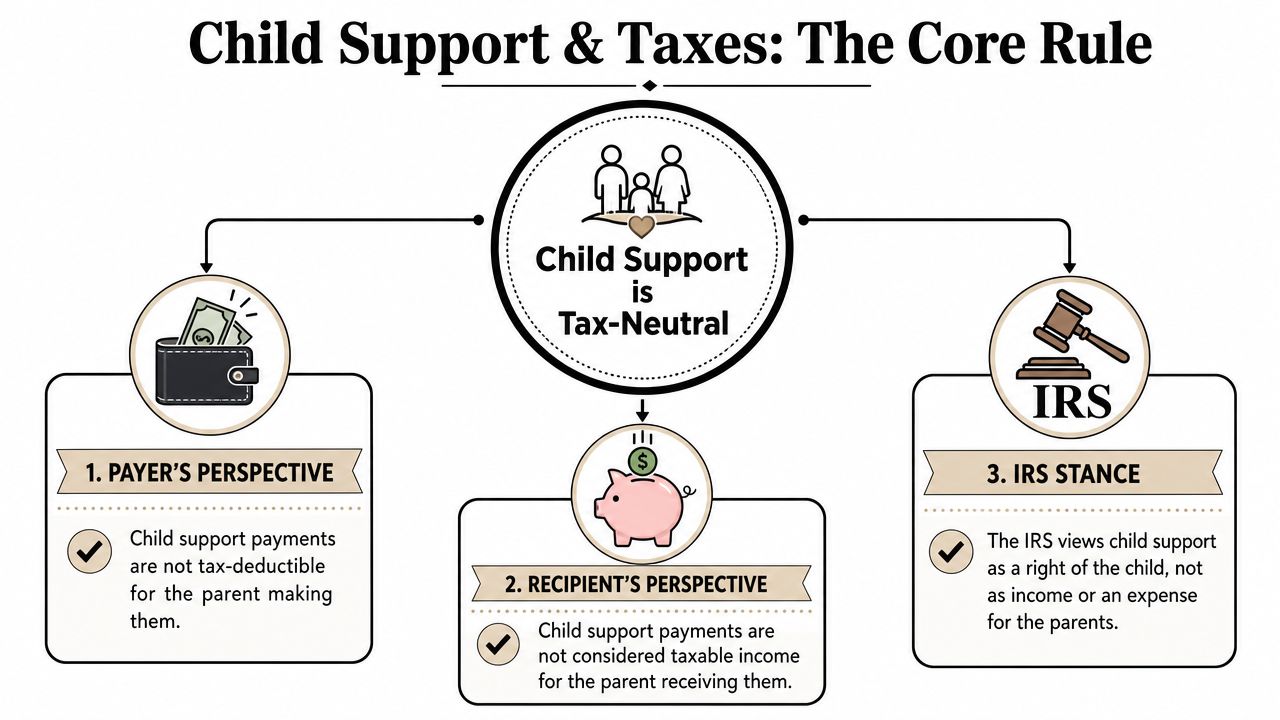

Child support payments aren’t deductible for the parent who pays them, and they aren’t taxable income for the parent who receives them.

If you’re staring at tax software, a divorce judgment, or a string of texts from an ex and wondering whether child support belongs anywhere on your return, you’re asking one of the most common post-separation tax questions. The confusion makes sense. Support payments, custody schedules, dependency claims, and changing IRS rules often get mashed together, especially during the first tax season after a divorce or breakup.

For Florida parents, the practical problem usually isn’t just understanding the federal rule. It’s making sure your parenting plan, marital settlement agreement, and tax documents all line up so nobody claims something they shouldn’t. That’s where avoidable disputes start. One parent assumes paying support means they get a tax break. The other assumes receiving support means they need to report it. Neither assumption is right.

The better approach is simple. Separate the questions. First, understand how the IRS treats child support. Then look at the separate issue of who may claim the child as a dependent. After that, make sure your Florida family law documents clearly spell out the tax terms so you don’t end up arguing with your ex, or explaining a messy record to the IRS.

Introduction Navigating Taxes After Divorce or Separation

The first tax season after a separation can feel oddly personal. You’re not just entering numbers. You’re revisiting the same issues that probably caused arguments before. Who paid what. Who had the child more often. Who gets to claim the child. Whether support counts as income.

A lot of parents type the same question into Google: can you claim child support payments on taxes? The answer is still no, but the reason matters because it affects how you organize your paperwork and how you talk about taxes with your ex-spouse or co-parent.

Think of child support and tax benefits as two different lanes. One lane is the payment itself. The other lane is the tax treatment tied to the child. People often merge those lanes and create trouble. A parent may believe, “I pay support, so I should get the deduction.” Another may think, “I receive support, so maybe I owe taxes on it.” Those are both common mistakes.

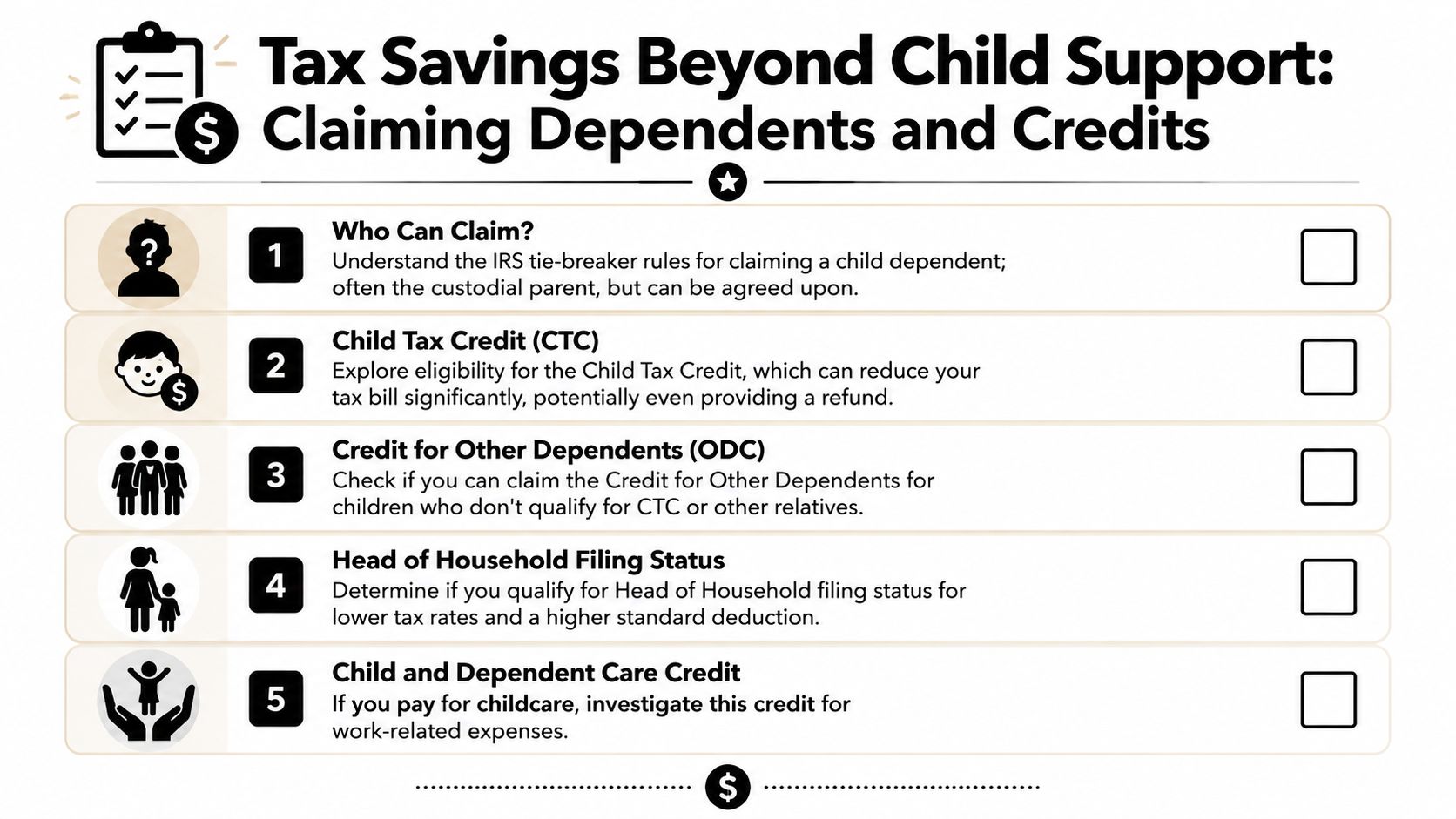

When parents confuse support with dependency rights, they often negotiate the wrong issue and document it badly.

For Florida families, this confusion shows up in settlement agreements, final judgments, and informal side agreements that were never written clearly. That’s where a federal tax rule collides with family law practice. The IRS has its own standards. Your court order has its own language. If the two don’t match, you’re left with a preventable mess.

The good news is that the basic rule is straightforward. The harder part is the follow-through. You need the right labels in the right places, and you need documents that say exactly who may claim what and when.

The Core Rule Child Support Is Tax-Neutral

A parent can pay child support every month for years and still get no federal tax deduction for it. A parent can receive that same money and still not report it as taxable income. That result feels counterintuitive until you separate family budgeting from tax classification.

Child support is tax-neutral. In plain terms, the payment does not lower the paying parent’s taxable income, and it does not raise the receiving parent’s taxable income.

Why the IRS doesn’t treat child support like income

The IRS views child support as money one parent is required to provide for the child’s benefit. It is not treated like wages paid to the receiving parent, and it is not treated like a deductible personal expense for the paying parent.

That distinction helps clear up a common point of confusion. In everyday life, child support absolutely affects cash flow. If you pay it, you feel the expense. If you receive it, you rely on it to help cover housing, food, school costs, and other needs. But federal tax law uses different labels than a household budget does. The tax question is narrower: does this payment fit a category the Internal Revenue Code taxes or allows as a deduction? Child support does not.

Practical rule: Do not report child support as income, and do not claim child support payments as a deduction on a federal return.

For Florida parents, this rule matters most when support terms are written into a marital settlement agreement, final judgment, or later modification. If an order mixes child support language with other payment obligations, confusion starts fast. Clear drafting helps prevent two separate problems. One is a dispute with your ex-spouse about what a payment was meant to cover. The other is a tax filing mistake that creates trouble later.